UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________________________________________

Form 10-K

___________________________________________________________

|

| |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2017

Commission File Number 0-7087

___________________________________________________________

Astronics Corporation

(Exact Name of Registrant as Specified in its Charter)

___________________________________________________________

|

| | |

New York | | 16-0959303 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

130 Commerce Way, East Aurora, N.Y. 14052

(Address of principal executive office)

Registrant’s telephone number, including area code (716) 805-1599

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

$.01 par value Common Stock; $.01 par value Class B Stock

(Title of Class)

___________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, an “accelerated filer”, a “non-accelerated filer” and a “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

Large accelerated filer | x | Accelerated filer | ¨ |

| | | |

Non-accelerated filer | ¨ | Smaller Reporting Company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of February 16, 2018, 28,066,764 shares were outstanding, consisting of 21,273,979 shares of Common Stock $.01 par value and 6,792,785 shares of Class B Stock $.01 par value. The aggregate market value, as of the last business day of the Company’s most recently completed second fiscal quarter, of the shares of Common Stock and Class B Stock of Astronics Corporation held by non-affiliates was approximately $731,000,000 (assuming conversion of all of the outstanding Class B Stock into Common Stock and assuming the affiliates of the Registrant to be its directors, executive officers and persons known to the Registrant to beneficially own more than 10% of the outstanding capital stock of the Corporation).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the 2018 Annual Meeting of Shareholders to be held May 31, 2018 are incorporated by reference into Part III of this Report.

Table of Contents

ASTRONICS CORPORATION

Index to Annual Report

on Form 10-K

Year Ended December 31, 2017

|

| | |

| | Page |

| | |

Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

| | |

| | |

Item 5. | | |

Item 6. | | |

Item 7. | | |

Item 7A. | | |

Item 8. | | |

Item 9. | | |

Item 9A. | | |

Item 9B. | | |

| | |

| | |

Item 10. | | |

Item 11. | | |

Item 12. | | |

Item 13. | | |

Item 14. | | |

| | |

| | |

Item 15. | | |

Item 16. | | |

FORWARD LOOKING STATEMENTS

Information included or incorporated by reference in this report that does not consist of historical facts, including statements accompanied by or containing words such as “may,” “will,” “should,” “believes,” “expects,” “expected,” “intends,” “plans,” “projects,” “approximate,” “estimates,” “predicts,” “potential,” “outlook,” “forecast,” “anticipates,” “presume” and “assume,” are forward-looking statements. Such forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements are not guarantees of future performance and are subject to several factors, risks and uncertainties, the impact or occurrence of which could cause actual results to differ materially from the expected results described in the forward-looking statements. Certain of these factors, risks and uncertainties are discussed in the sections of this report entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” New factors, risks and uncertainties may emerge from time to time that may affect the forward-looking statements made herein. Given these factors, risks and uncertainties, investors should not place undue reliance on forward-looking statements as predictive of future results. We disclaim any obligation to update the forward-looking statements made in this report.

PART I

ITEM 1. BUSINESS

Astronics Corporation (“Astronics” or the “Company”) is a leading provider of advanced technologies to the global aerospace, defense, electronics and semiconductor industries. Our products and services include advanced, high-performance electrical power generation, distribution and motion systems, lighting & safety systems, avionics products, aircraft structures, systems certification and automated test systems.

We have operations in the United States (“U.S.”), Canada and France. We design and build our products through our wholly owned subsidiaries Astronics Advanced Electronic Systems Corp. (“AES”); Astronics AeroSat Corporation (“AeroSat”); Armstrong Aerospace, Inc. (“Armstrong”); Astronics Test Systems, Inc. (“ATS”); Ballard Technology, Inc. (“Ballard”); Astronics Connectivity Systems and Certification Corp. (“CSC”); Astronics Custom Control Concepts Inc. (“CCC”); Astronics DME LLC (“DME”); Luminescent Systems, Inc. (“LSI”); Luminescent Systems Canada, Inc. (“LSI Canada”); Max-Viz, Inc. (“Max-Viz”); Peco, Inc. (“Peco”); and PGA Electronic s.a. (“PGA”).

Acquisitions

On January 14, 2015, the Company acquired all of the outstanding stock of Armstrong, located in Itasca, Illinois. Armstrong is a leading provider of engineering, design and certification solutions for commercial aircraft, specializing in connectivity, in-flight entertainment, and electrical power systems. Armstrong is included in our Aerospace segment.

On April 3, 2017, Astronics Custom Control Concepts Inc., a wholly owned subsidiary of the Company acquired substantially all the assets and certain liabilities of Custom Control Concepts LLC, located in Kent, Washington. CCC is a provider of cabin management and in-flight entertainment systems for a range of aircraft. The total consideration for the transaction was approximately $10.2 million, net of $0.5 million in cash acquired. CCC is included in our Aerospace segment.

On December 1, 2017, Astronics acquired substantially all of the assets of Telefonix Inc. and a related company, Product Development Technologies, LLC and its subsidiaries, to become CSC, primarily located in Waukegan and Lake Zurich, Illinois. CSC designs and manufactures advanced in-flight entertainment and connectivity equipment, and provides industry leading design consultancy services for the global aerospace industry. Under the terms of the Agreement, the total consideration for the transaction was approximately $103.8 million, net of $0.2 million in cash acquired. CSC is included in our Aerospace Segment.

Products and Customers

Our Aerospace segment designs and manufactures products for the global aerospace industry. Product lines include lighting and safety systems, electrical power generation, distribution and motions systems, aircraft structures, avionics products, systems certification, connectivity and other products. Our Aerospace customers are the airframe manufacturers (“OEM”) that build aircraft for the commercial, military and general aviation markets, suppliers to those OEM’s, aircraft operators such as airlines and branches of the U.S. Department of Defense as well as the Federal Aviation Administration and airport operators. During 2017, this segment’s sales were divided 78% to the commercial transport market, 11% to the military aircraft market, 8% to the business jet market and 3% to other markets. Most of this segment’s sales are a result of contracts or purchase orders received from customers, placed on a day-to-day basis or for single year procurements rather than long-term multi-year contract commitments. On occasion, the Company does receive contractual commitments or blanket purchase orders from our customers covering multiple-year deliveries of hardware to our customers.

Our Test Systems segment designs, develops, manufactures and maintains automated test systems that support the semiconductor, aerospace, communications and weapons test systems as well as training and simulation devices for both commercial and military applications. In the Test Systems segment, Astronics’ products are sold to a global customer base including OEMs and prime government contractors for both electronics and military products. During 2017, this segment’s sales were divided 36% to the semiconductor market and 64% to the aerospace & defense market.

Sales by segment, geographic region, major customer and foreign operations are provided in Note 17 of Item 8, Financial Statements and Supplementary Data in this report.

We have a significant concentration of business with two major customers; Panasonic Avionics Corporation (“Panasonic”) and The Boeing Company (“Boeing”). Sales to Panasonic accounted for 19.1% of sales in 2017, 21.6% of sales in 2016, and 21.0% of sales in 2015. Sales to Boeing accounted for 16.8% of sales in 2017, 15.2% of sales in 2016, and 13.0% of sales in 2015.

Strategy

Our strategy is to increase our value by developing technologies and capabilities either internally or through acquisition, and use those capabilities to provide innovative solutions to the aerospace & defense, semiconductor and other markets where our technology can be beneficial.

Practices as to Maintaining Working Capital

Liquidity is discussed in Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in the Liquidity and Capital Resources section of this report.

Competitive Conditions

We experience considerable competition in the market sectors we serve, principally with respect to product performance and price, from various competitors, many of which are substantially larger and have greater resources. Success in the markets we serve depends upon product innovation, customer support, responsiveness and cost management. We continue to invest in developing the technologies and engineering support critical to competing in our markets.

Government Contracts

All U.S. government contracts, including subcontracts where the U.S. government is the ultimate customer, may be subject to termination at the election of the government. Our revenue stream relies on military spending. Approximately 19% of our consolidated sales were made to the military aircraft and military test systems markets combined.

Raw Materials

Materials, supplies and components are purchased from numerous sources. We believe that the loss of any one source, although potentially disruptive in the short-term, would not materially affect our operations in the long-term.

Seasonality

Our business is typically not seasonal.

Backlog

At December 31, 2017, our backlog was $393.7 million million. At December 31, 2016, our backlog was $258.0 million. Backlog in the Aerospace segment was $298.6 million at December 31, 2017, of which $271.4 million is expected to be realized in 2018. Backlog in the Test Systems segment was $95.1 million at December 31, 2017, of which $75.3 million is expected to be realized in 2018.

Patents

We have a number of patents. While the aggregate protection of these patents is of value, our only material business that is dependent upon the protection afforded by these patents is our cabin power distribution products. Our patents and patent applications relate to electroluminescence, instrument panels, cord reels and handsets, and a broad patent covering the cabin power distribution technology. We regard our expertise and techniques as proprietary and rely upon trade secret laws and contractual arrangements to protect our rights. We have trademark protection in our major markets.

Research, Development and Engineering Activities

We are engaged in a variety of engineering and design activities as well as basic research and development activities directed to the substantial improvement or new application of our existing technologies. These costs are expensed when incurred and included in cost of sales. Research, development and engineering costs amounted to approximately $95.0 million in 2017, $88.9 million in 2016 and $90.3 million in 2015.

Employees

We employed approximately 2,500 employees at December 31, 2017. We consider our relations with our employees to be good. We have approximately 200 hourly production employees at Peco who are subject to collective bargaining agreements.

Available information

We file our financial information and other materials as electronically required with the Securities and Exchange Commission (“SEC”). These materials can be accessed electronically via the Internet at www.sec.gov. Such materials and other information about the Company are also available through our website at www.astronics.com.

ITEM 1A. RISK FACTORS

The loss of Panasonic or Boeing as major customers or a significant reduction in sales to either of those customers would reduce our sales and earnings. In 2017, we had a concentration of sales to Panasonic and Boeing representing approximately 19.1% and 16.8% of our sales, respectively. The loss of either of these customers or a significant reduction in sales to them would significantly reduce our sales and earnings.

The amount of debt we have outstanding, as well as any debt we may incur in the future, could have an adverse effect on our operational and financial flexibility. As of December 31, 2017, we had approximately $271.8 million of debt outstanding, of which $269.1 million is long-term debt. Changes to our level of debt subsequent to December 31, 2017 could have significant consequences to our business, including the following:

| |

• | Depending on interest rates and debt maturities, a substantial portion of our cash flow from operations could be dedicated to paying principal and interest on our debt, thereby reducing funds available for our acquisition strategy, capital expenditures or other purposes; |

| |

• | A significant amount of additional debt could make us more vulnerable to changes in economic conditions or increases in prevailing interest rates; |

| |

• | Our ability to obtain additional financing for acquisitions, capital expenditures or for other purposes could be impaired; |

| |

• | The increase in the amount of debt we have outstanding increases the risk of non-compliance with some of the covenants in our debt agreements which require us to maintain specified financial ratios; and |

| |

• | We may be more leveraged than some of our competitors, which may result in a competitive disadvantage. |

We are subject to debt covenant restrictions. Our credit facility contains several financial and other restrictive covenants. A significant decline in our operating income could cause us to violate our covenants. A covenant violation would require a waiver by the lenders or an alternative financing arrangement be achieved. This could result in our being unable to borrow under our bank credit facility or being obliged to refinance and renegotiate the terms of our bank indebtedness. Historically both choices have been available to us, however, it is difficult to predict the availability of these options in the future.

We are subject to financing and interest rate exposure risks that could adversely affect our business, liquidity and operating results. Changes in the availability, terms and cost of capital, and increases in interest rates could cause our cost of doing business to increase and place us at a competitive disadvantage. At December 31, 2017, approximately 4% of our debt was at fixed interest rates with the remainder subject to variable interest rates.

Our future operating results could be impacted by estimates used to calculate impairment losses on long lived assets. The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make significant and subjective estimates and assumptions that may affect the reported amounts of long lived assets in the financial statements. These estimates are integral in the determination of whether a potential non-cash impairment loss exists as well as the calculation of that loss. Actual future results could differ from those estimates.

A write-off of all or part of our goodwill or other intangible assets could adversely affect our operating results and net worth. At December 31, 2017, goodwill and purchased intangible assets were approximately 17.1% and 20.9% of our total assets, respectively. Our goodwill and other intangible assets may increase in the future since our strategy includes growing through acquisitions. We may have to write-off all or part of our goodwill or purchased intangible assets if their value becomes impaired. Although this write-off would be a non-cash charge, it could reduce our earnings and net worth significantly.

The markets we serve are cyclical and sensitive to domestic and foreign economic conditions and events, which may cause our operating results to fluctuate. Demand for our products is, to a large extent, dependent on the demand and success of our customers' products where we are a supplier to an OEM. In our Aerospace segment, demand by the business jet markets for our products is dependent upon several factors, including capital investment, product innovations, economic growth and wealth creation and technology upgrades. In addition, the commercial airline industry is highly cyclical and sensitive to fuel price increases, labor disputes, global economic conditions, availability of capital to fund new aircraft purchases and upgrades of existing aircraft and passenger demand. A change in any of these factors could result in a reduction in the amount of air travel and the ability of airlines to invest in new aircraft or to upgrade existing aircraft. These factors would reduce orders for new aircraft and would likely reduce airlines’ spending for cabin upgrades for which we supply products, thus reducing our sales and profits. A reduction in air travel may also result in our commercial airline customers being unable to pay our invoices on a timely basis or not at all.

We are a supplier on various new aircraft programs just entering or expected to begin production in the future. As with any new program, there is risk as to whether the aircraft or program will be successful and accepted by the market. As is customary for our business, we purchase inventory and invest in specific capital equipment to support our production requirements generally based on delivery schedules provided by our customer. If a program or aircraft is not successful, we may have to write-off all or a part of the inventory, accounts receivable and capital equipment related to the program. A write-off of these assets could result in a significant reduction of earnings and cause covenant violations relating to our debt agreements. This could result in our being unable to borrow additional funds under our bank credit facility or being obliged to refinance or renegotiate the terms of our bank indebtedness.

In our Test Systems segment, the market for our products is concentrated with a limited number of significant customers accounting for a substantial portion of the purchases of test equipment. In any one reporting period, a single customer or several customers may contribute an even larger percentage of our consolidated revenues. In addition, our ability to increase sales will depend, in part, on our ability to obtain orders from current or new significant customers. The opportunities to obtain orders from these customers may be limited, which may impair our ability to grow revenues. We expect that sales of our Test Systems products will continue to be concentrated with a limited number of significant customers for the foreseeable future. Additionally, demand for some of our test products is dependent upon government funding levels for our products, our ability to compete successfully for those contracts and our ability to develop products to satisfy the demands of our customers.

Our products are sold in highly competitive markets. Some of our competitors are larger, more diversified corporations and have greater financial, marketing, production and research and development resources. As a result, they may be better able to withstand the effects of periodic economic downturns. Our operations and financial performance will be negatively impacted if our competitors:

| |

• | develop products that are superior to our products; |

| |

• | develop products that are more competitively priced than our products; |

| |

• | develop methods of more efficiently and effectively providing products and services; or |

| |

• | adapt more quickly than we do to new technologies or evolving customer requirements. |

We believe that the principal points of competition in our markets are product quality, price, design and engineering capabilities, product development, conformity to customer specifications, quality of support after the sale, timeliness of delivery and effectiveness of the distribution organization. Maintaining and improving our competitive position will require continued investment in manufacturing, engineering, quality standards, marketing, customer service and support and our distribution networks. If we do not maintain sufficient resources to make these investments, or are not successful in maintaining our competitive position, our operations and financial performance will suffer.

Our future success depends to a significant degree upon the continued contributions of our management team and technical personnel. The loss of members of our management team could have a material and adverse effect on our business. In addition, competition for qualified technical personnel in our industry is intense, and we believe that our future growth and success will depend on our ability to attract, train and retain such personnel.

Future terror attacks, war, or other civil disturbances could negatively impact our business. Continued terror attacks, war or other disturbances could lead to economic instability and decreases in demand for our products, which could negatively impact our business, financial condition and results of operations. Terrorist attacks world-wide have caused instability from time to time in global financial markets and the aviation industry. The long-term effects of terrorist attacks on us are unknown. These attacks and the U.S. government’s continued efforts against terrorist organizations may lead to additional armed

hostilities or to further acts of terrorism and civil disturbance in the U.S. or elsewhere, which may further contribute to economic instability.

Our business and operations could be adversely impacted in the event of a failure of our information technology infrastructure or adversely impacted by a successful cyber-attack. We are dependent on various information technologies throughout our company to administer, store and support multiple business activities. We routinely experience various cybersecurity threats, threats to our information technology infrastructure, unauthorized attempts to gain access to our company sensitive information, and denial-of-service attacks as do our customers, suppliers and subcontractors. We conduct regular periodic training of our employees as to the protection of sensitive information which includes security awareness training intended to prevent the success of “phishing” attacks.

The threats we face vary from attacks common to most industries to more advanced and persistent, highly organized adversaries, including nation states, which target us and other defense contractors because we protect sensitive information. If we are unable to protect sensitive information, our customers or governmental authorities could question the adequacy of our threat mitigation and detection processes and procedures, and depending on the severity of the incident, our customers’ data, our employees’ data, our intellectual property, and other third party data (such as subcontractors, suppliers and vendors) could be compromised. As a consequence of their persistence, sophistication and volume, we may not be successful in defending against all such attacks. Due to the evolving nature of these security threats, the impact of any future incident cannot be predicted.

Although we work cooperatively with our customers, suppliers, and subcontractors to seek to minimize the impact of cyber threats, other security threats or business disruptions, we must rely on the safeguards put in place by these entities, which may affect the security of our information. These entities have varying levels of cyber security expertise and safeguards and their relationships with U.S. government contractors, such as Astronics, may increase the likelihood that they are targeted by the same cyber threats we face.

Our inability to adequately enforce and protect our intellectual property or defend against assertions of infringement could prevent or restrict our ability to compete. We rely on patents, trademarks and proprietary knowledge and technology, both internally developed and acquired, in order to maintain a competitive advantage. Our inability to defend against the unauthorized use of these rights and assets could have an adverse effect on our results of operations and financial condition. Litigation may be necessary to protect our intellectual property rights or defend against claims of infringement. This litigation could result in significant costs and divert our management’s focus away from operations.

If we are unable to adapt to technological change, demand for our products may be reduced. The technologies related to our products have undergone, and in the future may undergo, significant changes. To succeed in the future, we will need to continue to design, develop, manufacture, assemble, test, market and support new products and enhancements on a timely and cost effective basis. Our competitors may develop technologies and products that are more effective than those we develop or that render our technology and products obsolete or uncompetitive. Furthermore, our products could become unmarketable if new industry standards emerge. We may have to modify our products significantly in the future to remain competitive, and new products we introduce may not be accepted by our customers.

Our new product development efforts may not be successful, which would result in a reduction in our sales and earnings. We may experience difficulties that could delay or prevent the successful development of new products or product enhancements, and new products or product enhancements may not be accepted by our customers. In addition, the development expenses we incur may exceed our cost estimates, and new products we develop may not generate sales sufficient to offset our costs. If any of these events occur, our sales and profits could be adversely affected.

We depend on government contracts and subcontracts with defense prime contractors and sub-contractors that may not be fully funded, may be terminated, or may be awarded to our competitors. The failure to be awarded these contracts, the failure to receive funding or the termination of one or more of these contracts could reduce our sales. Sales to the U.S. government and its prime contractors and subcontractors represent a significant portion of our business. The funding of these programs is generally subject to annual congressional appropriations, and congressional priorities are subject to change. In addition, government expenditures for defense programs may decline or these defense programs may be terminated. A decline in governmental expenditures or the termination of existing contracts may result in a reduction in the volume of contracts awarded to us. We have resources applied to specific government contracts and if any of those contracts were terminated, we may incur substantial costs redeploying those resources.

If our subcontractors or suppliers fail to perform their contractual obligations, our prime contract performance and our ability to obtain future business could be materially and adversely impacted. Many of our contracts involve subcontracts with other companies upon which we rely to perform a portion of the services we must provide to our customers.

There is a risk that we may have disputes with our subcontractors, including disputes regarding the quality and timeliness of work performed by the subcontractor or customer concerns about the subcontractor. Failure by our subcontractors to satisfactorily provide, on a timely basis, the agreed-upon supplies or perform the agreed-upon services may materially and adversely impact our ability to perform our obligations with our customer. Subcontractor performance deficiencies could result in a customer terminating our contract for default. A default termination could expose us to liability and substantially impair our ability to compete for future contracts and orders. In addition, a delay in our ability to obtain components and equipment parts from our suppliers may affect our ability to meet our customers’ needs and may have an adverse effect upon our profitability.

Our results of operations are affected by our fixed-price contracts, which could subject us to losses in the event that we have cost overruns. For the year ended December 31, 2017, fixed-price contracts represented almost all of the Company’s sales. On fixed-price contracts, we agree to perform the scope of work specified in the contract for a predetermined price. Depending on the fixed price negotiated, these contacts may provide us with an opportunity to achieve higher profits based on the relationship between our costs and the contract’s fixed price. However, we bear the risk that increased or unexpected costs may reduce our profit.

Some of our contracts contain late delivery penalties. Failure to deliver in a timely manner due to supplier problems, development schedule slides, manufacturing difficulties, or similar schedule related events could have a material adverse effect on our business.

The failure of our products may damage our reputation, necessitate a product recall or result in claims against us that exceed our insurance coverage, thereby requiring us to pay significant damages. Defects in the design and manufacture of our products may necessitate a product recall. We include complex system design and components in our products that could contain errors or defects, particularly when we incorporate new technology into our products. If any of our products are defective, we could be required to redesign or recall those products or pay substantial damages or warranty claims. Such an event could result in significant expenses, disrupt sales and affect our reputation and that of our products. We are also exposed to product liability claims. We carry aircraft and non-aircraft product liability insurance consistent with industry norms. However, this insurance coverage may not be sufficient to fully cover the payment of any potential claim. A product recall or a product liability claim not covered by insurance could have a material adverse effect on our business, financial condition and results of operations.

Changes in discount rates and other estimates could affect our future earnings and equity. Our goodwill asset impairment evaluations are determined using valuations that involve several assumptions, including discount rates, cash flow estimates, growth rates and terminal values. Certain of these assumptions, particularly the discount rate, are based on market conditions and are outside of our control. Changes in these assumptions could affect our future earnings and equity.

Additionally, pension obligations and the related costs are determined using actual results and actuarial valuations that involve several assumptions. The most critical assumption is the discount rate. Other assumptions include mortality, salary increases and retirement age. The discount rate assumptions are based on current market conditions and are outside of our control. Changes in these assumptions could affect our future earnings and equity.

Contracting in the defense industry is subject to significant regulation, including rules related to bidding, billing and accounting kickbacks and false claims, and any non-compliance could subject us to fines and penalties or possible debarment. Like all government contractors, we are subject to risks associated with this contracting. These risks include the potential for substantial civil and criminal fines and penalties. These fines and penalties could be imposed for failing to follow procurement integrity and bidding rules, employing improper billing practices or otherwise failing to follow cost accounting standards, receiving or paying kickbacks or filing false claims. We have been, and expect to continue to be, subjected to audits and investigations by government agencies. The failure to comply with the terms of our government contracts could harm our business reputation. It could also result in suspension or debarment from future government contracts.

If we fail to meet expectations of securities analysts or investors due to fluctuations in our revenue or operating results, our stock price could decline significantly. Our revenue and earnings may fluctuate from quarter to quarter due to a number of factors, including delays or cancellations of programs. It is likely that in some future quarters our operating results may fall below the expectations of securities analysts or investors. In this event, the trading price of our stock could decline significantly.

Our operations in foreign countries expose us to political and currency risks and adverse changes in local legal and regulatory environments. In 2017, approximately 8.6% of our sales were made by our subsidiaries in France and Canada. Net assets held by these subsidiaries total $47.4 million at December 31, 2017. Our financial results may be adversely affected by

fluctuations in foreign currencies and by the translation of the financial statements of our foreign subsidiaries from local currencies into U.S. dollars. We expect international operations and export sales to continue to contribute to our earnings for the foreseeable future. Both the sales from international operations and export sales are subject in varying degrees to risks inherent in doing business outside of the U.S. Such risks include the possibility of unfavorable circumstances arising from host country laws or regulations, changes in tariff and trade barriers and import or export licensing requirements, and political or economic reprioritization, insurrection, civil disturbance or war.

Government regulations could limit our ability to sell our products outside the U.S. and could otherwise adversely affect our business. Certain of our sales are subject to compliance with U.S. export regulations. Our failure to obtain, or fully adhere to the limitations contained in, the requisite licenses, meet registration standards or comply with other government export regulations would hinder our ability to generate revenues from the sale of our products outside the U.S. Compliance with these government regulations may also subject us to additional fees and operating costs. The absence of comparable restrictions on competitors in other countries may adversely affect our competitive position. In order to sell our products in European Union countries, we must satisfy certain technical requirements. If we are unable to comply with those requirements with respect to a significant quantity of our products, our sales in Europe would be restricted. Doing business internationally also subjects us to numerous U.S. and foreign laws and regulations, including regulations relating to import-export control, technology transfer restrictions, foreign corrupt practices and anti-boycott provisions. Our failure, or failure by an authorized agent or representative that is attributable to us, to comply with these laws and regulations could result in administrative, civil or criminal liabilities and could, in the extreme case, result in monetary penalties, suspension or debarment from government contracts or suspension of our export privileges, which would have a material adverse effect on us.

Our stock price is volatile. For the year ended December 31, 2017, our stock price ranged from a low of $25.13 to a high of $43.87. The price of our common stock has been and likely will continue to be subject to wide fluctuations in response to a number of events and factors, such as:

| |

• | quarterly variations in operating results; |

| |

• | variances of our quarterly results of operations from securities analyst estimates; |

| |

• | changes in financial estimates; |

| |

• | announcements of technological innovations and new products; |

| |

• | news reports relating to trends in our markets; and |

| |

• | the cancellation of major contracts or programs with our customers. |

In addition, the stock market in general, and the market prices for companies in the aerospace & defense industry in particular, have experienced significant price and volume fluctuations that often have been unrelated to the operating performance of the companies affected by these fluctuations. These broad market fluctuations may adversely affect the market price of our common stock, regardless of our operating performance.

We may incur losses and liabilities as a result of our acquisition strategy. Growth by acquisition involves risks that could adversely affect our financial condition and operating results, including:

| |

• | diversion of management time and attention from our core business; |

| |

• | the potential exposure to unanticipated liabilities; |

| |

• | the potential that expected benefits or synergies are not realized and that operating costs increase; |

| |

• | the risks associated with incurring additional acquisition indebtedness, including that additional indebtedness could limit our cash flow availability for operations and our flexibility; |

| |

• | difficulties in integrating the operations and personnel of acquired companies; and |

| |

• | the potential loss of key employees, suppliers or customers of acquired businesses. |

In addition, any acquisition, once successfully integrated, could negatively impact our financial performance if it does not perform as planned, does not increase earnings, or does not prove otherwise to be beneficial to us.

We currently are involved or may become involved in the future, in legal proceedings that, if adversely adjudicated or settled, could materially impact our financial condition. As an aerospace company, we may become a party to litigation in the ordinary course of our business, including, among others, matters alleging product liability, warranty claims, breach of commercial or government contract or other legal actions. In general, litigation claims can be expensive and time consuming to bring or defend against and could result in settlements or damages that could significantly impact results of operations and financial condition.

We are a defendant in actions filed in the Regional State Court of Mannheim, Germany (Lufthansa Technik AG v. Astronics Advanced Electronics Systems Corp.) and the United States District for the Western District of Washington relating to an allegation of patent infringement. On December 29, 2010, Lufthansa Technik AG (“Lufthansa”) filed a Statement of Claim in the Regional State Court of Mannheim, Germany. Lufthansa’s claim asserts that our subsidiary, AES sold, marketed and brought into use in Germany a power supply system that infringes upon a German patent held by Lufthansa. The relief sought by Lufthansa includes requiring AES to stop selling and marketing the allegedly infringing power supply system, a recall of allegedly infringing products sold to commercial customers since November 26, 2003 and compensation for damages. The claim does not specify an estimate of damages and a damages claim will be made by Lufthansa only if it receives a favorable ruling on the determination of infringement.

On February 6, 2015, the Regional State Court of Mannheim, Germany rendered its decision that the patent was infringed. The judgment does not require AES to recall products that are already installed in aircraft or have been sold to other end users. On July 15, 2015, Lufthansa advised AES of their intention to enforce the accounting provisions of the decision, which required AES to provide certain financial information regarding sales of the infringing product to enable Lufthansa to make an estimate of requested damages. Additionally, if Lufthansa provides the required bank guarantee specified in the decision, the Company may be required to offer a recall of products that are in the distribution channels in Germany. No such bank guarantee has been issued to date. As of December 31, 2017 there are no products in the distribution channels in Germany.

The Company appealed to the Higher Regional Court of Karlsruhe. On November 15, 2016, the Court issued its ruling and upheld the lower court’s decision. The Company has submitted a petition to grant AES leave for appeal to the Federal Supreme Court. The Company believes it has valid defenses to refute the decision. Should the Federal Supreme Court decide to hear the case, the appeal process is estimated to extend up to two years. We estimate AES’s potential exposure related to this matter to be approximately $1 million to $3 million. As loss exposure is not probable at this time, the Company has not recorded any liability with respect to this litigation as of December 31, 2017.

In December 2017, Lufthansa filed patent infringement cases in the United Kingdom and in France against AES. AES has been served in the case in France, but not in the case in the United Kingdom. In those cases, Lufthansa accuses AES of manufacturing, using, selling and offering for sale a power supply system that infringes upon a Lufthansa patent in those respective countries. As loss exposure is neither probable nor estimable at this time, the Company has not recorded any liability with respect to this litigation as of December 31, 2017.

Other than these proceedings, we are not party to any significant pending legal proceedings that management believes will result in a material adverse effect on our financial condition or results of operations.

| |

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None

ITEM 2. PROPERTIES

On December 31, 2017, we own or lease 1.2 million square feet of space in the U.S., Canada and France, distributed as follows:

|

| | | | | | | | |

| Owned | | Leased | | Total |

Aerospace: | | | | | |

Clackamas, OR | 237,000 |

| | — |

| | 237,000 |

|

Kirkland, WA | 97,000 |

| | 39,000 |

| | 136,000 |

|

East Aurora, NY | 125,000 |

| | — |

| | 125,000 |

|

Ft. Lauderdale, FL | 96,000 |

| | — |

| | 96,000 |

|

Lebanon, NH | 83,000 |

| | — |

| | 83,000 |

|

Montierchaume, France* | — |

| | 80,000 |

| | 80,000 |

|

Itasca, IL | 49,000 |

| | — |

| | 49,000 |

|

Amherst, NH | — |

| | 28,000 |

| | 28,000 |

|

Montreal, Quebec, Canada | — |

| | 25,000 |

| | 25,000 |

|

Everett, WA | — |

| | 22,000 |

| | 22,000 |

|

Chicago, IL | — |

| | 2,000 |

| | 2,000 |

|

Kent, WA | — |

| | 65,000 |

| | 65,000 |

|

Waukegan, IL | — |

| | 41,000 |

| | 41,000 |

|

Lake Zurich, IL | — |

| | 36,000 |

| | 36,000 |

|

Lviv City, Ukraine | — |

| | 6,000 |

| | 6,000 |

|

Wheatley, Oxfordshire, UK | — |

| | 3,000 |

| | 3,000 |

|

Carlsbad, CA | — |

| | 1,000 |

| | 1,000 |

|

Aerospace Square Feet | 687,000 |

| | 348,000 |

| | 1,035,000 |

|

Test Systems: | | | | | |

Irvine, CA* | — |

| | 99,000 |

| | 99,000 |

|

Orlando, FL | — |

| | 51,000 |

| | 51,000 |

|

Test Systems Square Feet | — |

| | 150,000 |

| | 150,000 |

|

Total Square Feet | 687,000 |

| | 498,000 |

| | 1,185,000 |

|

* - Capitalized leases.

Upon the expiration of our current leases, we believe that we will be able to either secure renewal terms or enter into leases for or purchases of alternative locations at market terms. We believe that our properties have been adequately maintained and are generally in good condition.

On December 29, 2010, Lufthansa Technik AG (“Lufthansa”) filed a Statement of Claim in the Regional State Court of Mannheim, Germany. Lufthansa’s claim asserts that our subsidiary, AES sold, marketed and brought into use in Germany a power supply system that infringes upon a German patent held by Lufthansa. The relief sought by Lufthansa includes requiring AES to stop selling and marketing the allegedly infringing power supply system, a recall of allegedly infringing products sold to commercial customers since November 26, 2003 and compensation for damages. The claim does not specify an estimate of damages and a damages claim will be made by Lufthansa only if it receives a favorable ruling on the determination of infringement.

On February 6, 2015, the Regional State Court of Mannheim, Germany rendered its decision that the patent was infringed. The judgment does not require AES to recall products that are already installed in aircraft or have been sold to other end users. On July 15, 2015, Lufthansa advised AES of their intention to enforce the accounting provisions of the decision, which required AES to provide certain financial information regarding sales of the infringing product to enable Lufthansa to make an estimate of requested damages. Additionally, if Lufthansa provides the required bank guarantee specified in the decision, the Company may be required to offer a recall of products that are in the distribution channels in Germany. No such bank guarantee has been issued to date. As of December 31, 2017, there are no products in the distribution channels in Germany.

The Company appealed to the Higher Regional Court of Karlsruhe. On November 15, 2016, the Court issued its ruling and upheld the lower court’s decision. The Company has submitted a petition to grant AES leave for appeal to the Federal Supreme Court. The Company believes it has valid defenses to refute the decision. Should the Federal Supreme Court decide to hear the case, the appeal process is estimated to extend up to two years. We estimate AES’s potential exposure related to this matter to be approximately $1 million to $3 million. As loss exposure is not probable at this time, the Company has not recorded any liability with respect to this litigation as of December 31, 2017.

On November 26, 2014, Lufthansa filed a complaint in the United States District for the Western District of Washington. Lufthansa’s complaint in this action alleges that AES manufactures, uses, sells and offers for sale a power supply system that infringes upon a U.S. patent held by Lufthansa. The patent at issue in the U.S. action is based on technology similar to that involved in the German action. On April 25, 2016, the Court issued its ruling on claim construction, holding that the sole independent claim in the patent is indefinite, rendering all claims in the patent indefinite. Based on this ruling, AES filed a motion for summary judgment on the grounds that the Court’s ruling that the patent is indefinite renders the patent invalid and unenforceable. On July 20, 2016, the U.S. District Court granted the motion for summary judgment and issued an order dismissing all claims against AES with prejudice. Lufthansa appealed the District Court's decision to the United States Court of Appeals for the Federal Circuit. On October 19, 2017, the Federal Circuit affirmed the District Court's decision, holding that the sole independent claim of the patent is indefinite, rendering all claims on the patent indefinite. Lufthansa did not file a petition for en banc rehearing or petition the U.S. Supreme Court for a writ of certiorari. Therefore, there is no longer a risk of exposure from that lawsuit.

In December 2017, Lufthansa filed patent infringement cases in the United Kingdom and in France against AES. AES has been served in the case in France, but not in the case in the United Kingdom. In those cases, Lufthansa accuses AES of manufacturing, using, selling and offering for sale a power supply system that infringes upon a Lufthansa patent in those respective countries. As loss exposure is neither probable nor estimable at this time, the Company has not recorded any liability with respect to this litigation as of December 31, 2017.

| |

ITEM 4. | MINE SAFETY DISCLOSURES |

Not Applicable

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The table below sets forth the range of prices for the Company’s Common Stock, traded on the NASDAQ National Market System, for each quarterly period during the last two years. The approximate number of shareholders of record as of February 16, 2018, was 811 for Common Stock and 2,112 for Class B Stock.

|

| | | | | | | |

2017 | High | | Low |

First | $ | 34.77 |

| | $ | 28.79 |

|

Second | $ | 33.29 |

| | $ | 29.73 |

|

Third | $ | 31.44 |

| | $ | 25.13 |

|

Fourth | $ | 43.87 |

| | $ | 30.15 |

|

|

| | | | | | | |

2016 | High | | Low |

First | $ | 34.55 |

| | $ | 21.76 |

|

Second | $ | 34.22 |

| | $ | 27.65 |

|

Third | $ | 39.17 |

| | $ | 28.05 |

|

Fourth | $ | 40.70 |

| | $ | 30.76 |

|

The Company has not paid any cash dividends in the three-year period ended December 31, 2017. The Company has no plans to pay cash dividends as it plans to retain all cash from operations as a source of capital to finance growth in the business.

On September 26, 2016, the Company announced a three-for-twenty distribution of Class B Stock to holders of both Common and Class B Stock. Stockholders received three shares of Class B Stock for every twenty shares of Common and Class B Stock held on the record date of October 11, 2016. Fractional shares were paid in cash. All share quantities, share prices and per share data reported throughout this report have been adjusted to reflect the impact of this distribution.

On February 24, 2016, the Company’s Board of Directors authorized the repurchase of up to $50 million of common stock (the “Buyback Program”). The Buyback Program allowed the Company to purchase shares of its common stock in accordance with applicable securities laws on the open market or through privately negotiated transactions. The Company has repurchased approximately 1,675,000 shares and has completed that program. On December 12, 2017, the Company’s Board of Directors authorized an additional repurchase of up to $50 million of common stock. No amounts have been repurchased under the new program as of December 31, 2017.

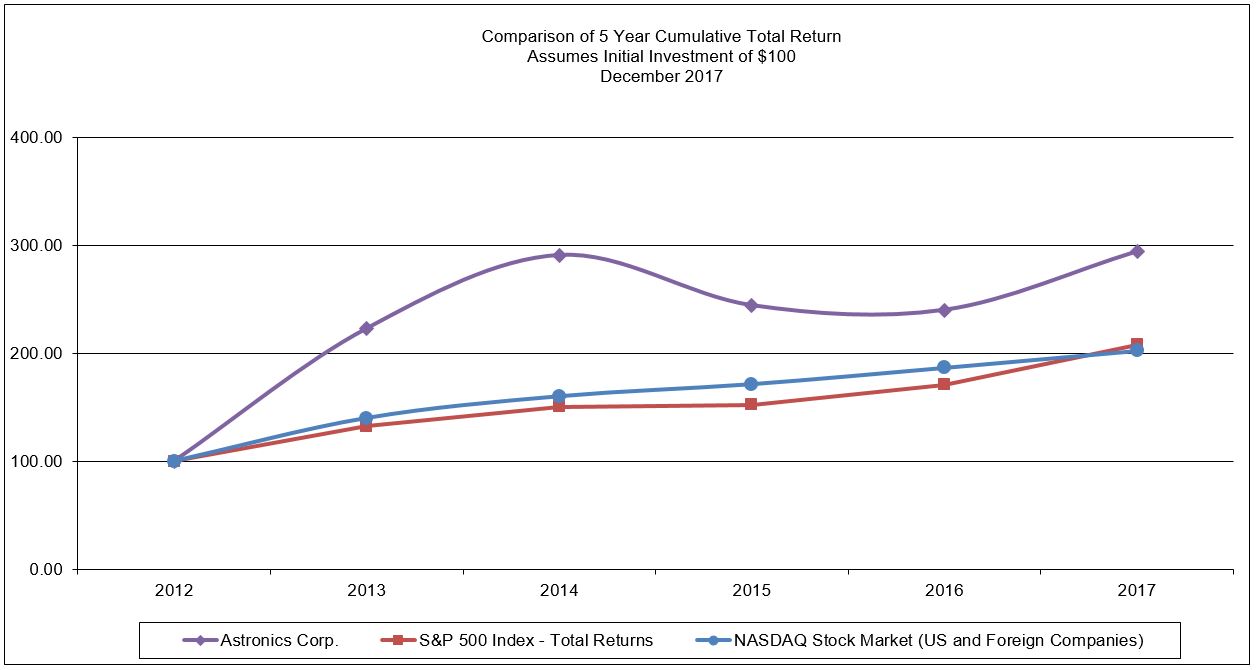

The following graph and table shows the performance of the Company’s common stock compared with the S&P 500 Index — Total Return and the NASDAQ US and Foreign Companies for a $100 investment made December 31, 2012:

|

| | | | | | | | | | | | | | | | | | |

| | 2012 | | 2013 | | 2014 | | 2015 | | 2016 | | 2017 |

Astronics Corp. | Return % | — |

| | 122.90 |

| | 30.51 |

| | (15.99 | ) | | (1.75 | ) | | 22.55 |

|

| Cum $ | 100.00 |

| | 222.90 |

| | 290.91 |

| | 244.38 |

| | 240.11 |

| | 294.24 |

|

S&P 500 Index - Total Returns | Return % | — |

| | 32.39 |

| | 13.69 |

| | 1.38 |

| | 11.96 |

| | 21.83 |

|

| Cum $ | 100.00 |

| | 132.39 |

| | 150.51 |

| | 152.59 |

| | 170.84 |

| | 208.14 |

|

NASDAQ Stock Market (US and Foreign Companies) | Return % | — |

| | 40.10 |

| | 14.43 |

| | 6.99 |

| | 8.82 |

| | 8.43 |

|

| Cum $ | 100.00 |

| | 140.10 |

| | 160.32 |

| | 171.53 |

| | 186.65 |

| | 202.39 |

|

ITEM 6. SELECTED FINANCIAL DATA

Five-Year Performance Highlights

|

| | | | | | | | | | | | | | | | | | | |

| 2017 (5) | | 2016 | | 2015 (4) | | 2014 (3) | | 2013 (2) |

(Amounts in thousands, except for employee and per share data) | | | | | | | | | |

RESULTS OF OPERATIONS: | | | | | | | | | |

Sales | $ | 624,464 |

| | $ | 633,123 |

| | $ | 692,279 |

| | $ | 661,039 |

| | $ | 339,937 |

|

Net Income | $ | 19,679 |

| | $ | 48,424 |

| | $ | 66,974 |

| | $ | 56,170 |

| | $ | 27,266 |

|

Impairment Loss (6) | $ | 16,237 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

|

Net Margin | 3.2 | % | | 7.6 | % | | 9.7 | % | | 8.5 | % | | 8.0 | % |

Diluted Earnings Per Share (1) | $ | 0.67 |

| | $ | 1.61 |

| | $ | 2.22 |

| | $ | 1.87 |

| | $ | 0.94 |

|

Weighted Average Shares Outstanding – Diluted (1) | 29,320 |

| | 30,032 |

| | 30,179 |

| | 29,970 |

| | 29,136 |

|

Return on Average Equity | 5.9 | % | | 15.2 | % | | 25.3 | % | | 28.1 | % | | 18.4 | % |

YEAR-END FINANCIAL POSITION: | | | | | | | | | |

Working Capital | $ | 212,438 |

| | $ | 168,513 |

| | $ | 145,735 |

| | $ | 136,602 |

| | $ | 125,961 |

|

Total Assets | $ | 735,956 |

| | $ | 604,344 |

| | $ | 609,243 |

| | $ | 562,910 |

| | $ | 491,271 |

|

Indebtedness | $ | 271,767 |

| | $ | 148,120 |

| | $ | 169,789 |

| | $ | 183,008 |

| | $ | 200,320 |

|

Shareholders’ Equity | $ | 329,927 |

| | $ | 337,449 |

| | $ | 300,225 |

| | $ | 228,177 |

| | $ | 171,509 |

|

Book Value Per Share (1) | $ | 11.77 |

|

| $ | 11.60 |

|

| $ | 10.21 |

|

| $ | 7.87 |

|

| $ | 6.05 |

|

OTHER YEAR-END DATA: | | | | | | | | | |

Depreciation and Amortization | $ | 27,063 |

| | $ | 25,790 |

| | $ | 25,309 |

| | $ | 27,254 |

| | $ | 11,059 |

|

Capital Expenditures | $ | 13,478 |

| | $ | 13,037 |

| | $ | 18,641 |

| | $ | 40,882 |

| | $ | 6,868 |

|

Shares Outstanding (1) | 28,038 |

| | 29,098 |

| | 29,405 |

| | 29,003 |

| | 28,342 |

|

Number of Employees | 2,516 |

| | 2,304 |

| | 2,304 |

| | 2,041 |

| | 1,715 |

|

| |

(1) - | Diluted Earnings Per Share, Weighted Average Shares Outstanding - Diluted, Book Value Per Share and Shares Outstanding have been adjusted for the impact of the October 11, 2016 fifteen percent Class B stock distribution, October 8, 2015 fifteen percent Class B stock distribution, the September 5, 2014 twenty percent Class B stock distribution and the October 10, 2013 twenty percent Class B stock distribution. |

| |

(2) - | Information includes the results of Peco, acquired on July 18, 2013, AeroSat acquired on October 1, 2013 and PGA acquired December 5, 2013, each from the acquisition date forward. |

| |

(3) - | Information includes the results of ATS, acquired on February 28, 2014, from the acquisition date forward. |

| |

(4) - | Information includes the results of Armstrong, acquired on January 14, 2015, from the acquisition date forward. |

| |

(5) - | Information includes the results of CCC acquired on April 3, 2017 and CSC acquired December 1, 2017, each from the acquisition date forward. |

| |

(6) - | The Company recorded a $16.2 million goodwill impairment charge during the fourth quarter of 2017. Refer to “Item 7. Management’s Discussion and Analysis of Results of Operations and Financial Condition” and Note 5 of our consolidated financial statements for additional information on Goodwill. |

| |

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

OVERVIEW

Astronics, through its subsidiaries, designs and manufactures advanced, high-performance electrical power generation, distribution and motion systems, lighting & safety systems, avionics products, aircraft structures, systems certification and automated test systems.

Our strategy is to increase our value by developing technologies and capabilities either internally or through acquisition, and use those capabilities to provide innovative solutions to the aerospace & defense, semiconductor and other markets where our technology can be beneficial.

We have two reportable segments, Aerospace and Test Systems. Our Aerospace segment has thirteen principal operating facilities with one located in New York State, Florida, Oregon, Quebec, Canada and Montierchaume, France; two located in

New Hampshire; and three located in each of Illinois and Washington State. Our Test Systems segment has facilities located in Florida and California.

Our Aerospace segment serves three primary markets. They are the military, commercial transport and business jet markets. Our Test Systems segment serves the aerospace & defense and semiconductor markets.

Important factors affecting our growth and profitability are the rate at which new aircraft are produced, government funding of military programs, our ability to have our products designed into new aircraft and the rates at which aircraft owners, including commercial airlines, refurbish or install upgrades to their aircraft. New aircraft build rates and aircraft owners spending on upgrades and refurbishments is cyclical and dependent on the strength of the global economy. Once designed into a new aircraft, the spare parts business is frequently retained by the Company. Future growth and profitability of the test business is dependent on developing and procuring new and follow-on business in the semiconductor market as well as with the military. The nature of our test systems business is such that it pursues large multi-year projects. There can be significant periods of time between orders in this business which may result in large fluctuations of sales and profit levels and backlog from period to period.

Each of the markets that we serve presents opportunities that we expect will provide growth for the Company over the long-term. We continue to look for opportunities in all of our markets to capitalize on our core competencies to expand our existing business and to grow through strategic acquisitions.

Challenges which continue to face us include improving shareholder value through increasing profitability. Increasing profitability is dependent on many things, primarily revenue growth and the Company’s ability to control operating expenses and to identify means of creating improved productivity. Revenue is driven by increased build rates for existing aircraft, market acceptance and economic success of new aircraft and our products, continued government funding of defense programs, the Company’s ability to obtain production contracts for parts we currently supply or have been selected to design and develop for new aircraft platforms and continually identifying and winning new business for our Test Systems segment. Our semiconductor test products are highly dependent on winning new and follow-on programs with our current customers as well as developing new customers. Reduced aircraft build rates driven by a weak economy, tight credit markets, reduced air passenger travel and an increasing supply of used aircraft on the market would likely result in reduced demand for our products, which will result in lower profits. Reduction of defense spending may result in fewer opportunities for us to compete, which could result in lower profits in the future. Many of our newer development programs are based on new and unproven technology and at the same time we are challenged to develop the technology on a schedule that is consistent with specific programs. We will continue to address these challenges by working to improve operating efficiencies and focusing on executing on the growth opportunities currently in front of us.

ACQUISITIONS

On December 1, 2017, Astronics acquired substantially all of the assets of Telefonix Inc. and a related company Product Development Technologies, LLC and its subsidiaries, to become CSC, located primarily in Waukegan and Lake Zurich, Illinois. CSC designs and manufactures advanced in-flight entertainment and connectivity equipment, and provides industry leading design consultancy services for the global aerospace industry. Under the terms of the Agreement, the total consideration for the transaction was approximately $103.8 million, net of $0.2 million in cash acquired. CSC is included in our Aerospace Segment.

On April 3, 2017, Astronics Custom Control Concepts Inc., a wholly owned subsidiary of the Company acquired substantially all the assets and certain liabilities of CCC, located in Kent, Washington. CCC is a provider of cabin management and in-flight entertainment systems for a range of aircraft. The total consideration for the transaction was approximately $10.2 million, net of $0.5 million in cash acquired. CCC is included in our Aerospace segment.

On January 14, 2015, the Company purchased 100% of the equity of Armstrong for approximately $52.3 million in cash. Armstrong, located in Itasca, Illinois, is a leading provider of engineering, design and certification solutions for commercial aircraft, specializing in connectivity, in-flight entertainment, and electrical power systems. Armstrong is included in our Aerospace segment.

MARKETS

Commercial Transport Market

Sales to the commercial transport market include sales of electrical power generation, distribution and motion products, lighting & safety products, avionics products, systems certification and structures products. Sales to this market totaled approximately $414.5 million or 66.4% of our consolidated sales in 2017.

Maintaining and growing sales to the commercial transport market will depend on airlines’ capital spending budgets for cabin upgrades as well as the purchase of new aircraft by global airlines. This spending by the airlines is impacted by their profits, cash flow and available financing as well as competitive pressures between the airlines to improve the travel experience for their passengers. We expect that new aircraft will be equipped with more passenger and aircraft connectivity and in-seat power than previous generation aircraft. This market has experienced strong growth from airlines installing in-seat passenger power systems on their existing and newly delivered aircraft. Our ability to maintain and grow sales to this market depends on our ability to maintain our technological advantages over our competitors and maintain our relationships with major in-flight entertainment suppliers and global airlines.

Military Aerospace Market

Sales to the military aerospace market include sales of lighting & safety products, avionics products, electrical power & motion products and other products. Sales to this market totaled approximately 9.8% of our consolidated revenue and amounted to $61.3 million in 2017.

The military market is dependent on governmental funding which can change from year to year. Risks are that overall spending may be reduced in the future, specific programs may be eliminated or that we fail to win new business through the competitive bid process. Astronics does not have significant reliance on any one program such that cancellation of a particular program will cause material financial loss. We believe that we will continue to have opportunities similar to past years regarding this market.

Business Jet Market

Sales to the business jet aerospace market include sales of lighting & safety products, avionics products, and electrical power & motion products. Sales to this market totaled approximately 6.6% of our consolidated revenue in 2017 and amounted to $41.3 million.

Sales to the business jet market are driven by our ship set content on new aircraft and build rates of new aircraft. Business jet OEM build rates continue to be significantly impacted by slow global wealth creation and corporate profitability which have been negatively affected during the past several years by global economic uncertainty among prospective buyers. Our sales to the business jet market will continue to be challenged in the upcoming year as business jet aircraft production rates are not expected to increase significantly during 2018. Despite the current market conditions, we continue to see opportunities on new aircraft currently in the design phase to employ our lighting & safety, electrical power and avionics technologies in the business jet market. There is risk involved in the development of any new aircraft including the risk that the aircraft will not ultimately be produced or that it will be produced in lower quantities than originally expected and thus impacting our return on our engineering and development efforts.

Other Aerospace

Sales of our other aerospace products include sales of airfield lighting products and other Peco products. Sales to this market totaled approximately 2.8% of our total revenue or $17.5 million in 2017.

Tests Systems Products

Our Test Systems segment accounted for approximately 14.4% of our consolidated sales in 2017 and amounted to $89.9 million. Sales to the semiconductor market were approximately $32.0 million. Sales to the aerospace & defense market were approximately $57.9 million in 2017.

CRITICAL ACCOUNTING POLICIES

Our financial statements and accompanying notes are prepared in accordance with U.S. generally accepted accounting principles. The preparation of the Company’s financial statements requires management to make estimates, assumptions and judgments that affect the amounts reported. These estimates, assumptions and judgments are affected by management’s

application of accounting policies, which are discussed in the Notes to Consolidated Financial Statements, Note 1 of Item 8, Financial Statements and Supplementary Data of this report. The critical accounting policies have been reviewed with the Audit Committee of our Board of Directors.

Revenue Recognition

The vast majority of our sales agreements are for standard products and services, with revenue recognized on the accrual basis at the time of shipment of goods, transfer of title and customer acceptance, where required. There are no significant contracts allowing for right of return. To a limited extent, certain contracts involve multiple elements (such as equipment and service). The Company recognizes revenue for delivered elements when they have stand-alone value to the customer, they have been accepted by the customer, and for which there are only customary refund or return rights. Arrangement consideration is allocated to the deliverables by use of the relative selling price method. The selling price used for each deliverable is based on vendor-specific objective evidence (“VSOE”) if available, third party-evidence (“TPE”) if VSOE is not available, or estimated selling price if neither VSOE nor TPE is available. Estimated selling price is determined in a manner consistent with that used to establish the price to sell the deliverable on a standalone basis.

For prepaid service contracts, sales revenue is recognized on a straight-line basis over the term of the contract, unless historical evidence indicates the costs are incurred on other than a straight-line basis.

Revenue of approximately $21.0 million, $20.7 million and $17.2 million for the years ended December 31, 2017, 2016 and 2015, respectively, was recognized from long-term, fixed-price contracts using the percentage-of-completion method of accounting, measured by multiplying the estimated total contract value by the ratio of actual contract costs incurred to date to the estimated total contract costs. The Company makes significant estimates involving its usage of percentage-of-completion accounting to recognize contract revenues. The Company periodically reviews contracts in process for estimates-to-completion, and revises estimated gross profit accordingly. While the Company believes its estimated gross profit on contracts in process is reasonable, unforeseen events and changes in circumstances can take place in a subsequent accounting period that may cause the Company to revise its estimated gross profit on one or more of its contracts in process. Accordingly, the ultimate gross profit realized upon completion of such contracts can vary significantly from estimated amounts between accounting periods. For contracts with anticipated losses at completion, a charge is taken against income for the amount of the entire loss in the period in which it is estimated.

Reviews for Impairment of Long-Lived Assets

Goodwill Impairment Testing

Our goodwill is the result of the excess of purchase price over net assets acquired from acquisitions. As of December 31, 2017, we had approximately $125.6 million of goodwill. As of December 31, 2016, we had approximately $115.2 million of goodwill. The change in goodwill is primarily due to the goodwill recorded associated with the acquisitions of CCC and CSC of $2.3 million and $23.4 million, respectively, offset by a goodwill impairment of $16.2 million at Armstrong.

We identify our reporting units by assessing whether the components of our operating segments constitute businesses for which discrete financial information is available and segment management regularly reviews the operating results of those components. The Test Systems operating segment is its own reporting unit while the other reporting units are one level below our Aerospace operating segment.

Companies may perform a qualitative assessment as the initial step in the annual goodwill impairment testing process for all or selected reporting units under certain circumstances. Companies are also allowed to bypass the qualitative analysis and perform a quantitative analysis if desired. Economic uncertainties and the length of time from the calculation of a baseline fair value are factors that we would consider in determining whether to perform a quantitative test.

When we evaluate the potential for goodwill impairment using a qualitative assessment, we consider factors including, but not limited to, macroeconomic conditions, industry conditions, the competitive environment, changes in the market for our products and services, regulatory and political developments, entity specific factors such as strategy and changes in key personnel and overall financial performance. If, after completing this assessment, it is determined that it is more likely than not that the fair value of a reporting unit is less than its carrying value, we proceed to a quantitative two-step impairment test.

Quantitative testing first requires a comparison of the fair value of each reporting unit to the carrying value. We use the discounted cash flow method to estimate the fair value of each of our reporting units. The discounted cash flow method incorporates various assumptions, the most significant being projected revenue growth rates, operating profit margins and cash

flows, the terminal growth rate and the discount rate. Management projects revenue growth rates, operating margins and cash flows based on each reporting unit’s current business, expected developments and operational strategies. If the carrying value of the reporting unit exceeds its fair value, goodwill is considered impaired and any loss must be measured. We early adopted ASU No. 2017-04 on January 1, 2017. Accordingly, goodwill impairment is measured as the amount by which a reporting unit's carrying value exceeds its fair value, not to exceed the carrying value of goodwill.

In 2017, we performed quantitative assessments for the nine reporting units which had goodwill as of the first day of the fourth quarter. Based on our quantitative assessments of our reporting units, the Company recorded a full impairment charge of approximately $16.2 million in the December 31, 2017 consolidated statement of operations associated to the Armstrong reporting unit. The impairment loss was incurred in the Aerospace segment and is reported on the Impairment Loss line of the Consolidated Statements of Operations.

Amortized Intangible Asset Impairment Testing

Amortizable intangible assets with a carrying value of $153.5 million at December 31, 2017 and $98.1 million at December 31, 2016 are amortized over their assigned useful lives. We test these long-lived assets for impairment when events or changes in circumstances indicate that the carrying amount of those assets may not be recoverable. The recoverability test consists of comparing the projected undiscounted cash flows associated with the asset to its carrying amount. An impairment loss would then be recognized for the carrying amount in excess of its fair value. There were no impairment charges in 2017, 2016 or 2015.

Depreciable Asset Impairment Testing

Property, plant and equipment with a carrying value of $125.8 million at December 31, 2017 and $122.8 million at December 31, 2016 are depreciated over their assigned useful lives. We test these long-lived assets for impairment when events or changes in circumstances indicate that the carrying amount of those assets may not be recoverable. The recoverability test consists of comparing the projected undiscounted cash flows, with its carrying amount. An impairment loss would then be recognized for the carrying amount in excess of its fair value. There were no impairment charges in 2017, 2016 or 2015.

Inventory Valuation

We record valuation reserves to provide for excess, slow moving or obsolete inventory or to reduce inventory to the lower of cost or net realizable value. In determining the appropriate reserve, management considers the age of inventory on hand, the overall inventory levels in relation to forecasted demands as well as reserving for specifically identified inventory that we believe is no longer salable. At December 31, 2017, our reserve for inventory valuation was $18.0 million, or 10.7% of gross inventory. At December 31, 2016, our reserve for inventory valuation was $15.4 million, or 11.7% of gross inventory.

Deferred Tax Asset Valuation Allowances

Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. We record a valuation allowance to reduce deferred tax assets to the amount of future tax benefit that we believe is more likely than not to be realized. Significant assumptions regarding future profitability is required to estimate the value of these deferred tax assets. We consider allowable tax carryforward periods, historical earnings performance, tax planning strategies and recent earnings projections to determine the amount of the valuation allowance. Changes in these factors could cause us to adjust our valuation allowance, which would impact our income tax expense and the carrying value of these assets when we determine that these factors have changed.

As of December 31, 2017, we had net deferred tax liabilities of $2.3 million. Included in the net deferred tax liabilities are approximately $15.4 million in deferred tax assets net of a $7.8 million valuation allowance. These deferred tax assets principally relate to employee benefit liabilities, asset reserves, leases, deferred revenue, state and foreign net operating loss carry-forwards, and state general business tax credit carry-forwards.

As of December 31, 2016, we had net deferred tax liabilities of $8.7 million. Included in the net deferred tax liabilities are approximately $24.2 million in deferred tax assets net of a $3.8 million valuation allowance. These deferred tax assets principally relate to employee benefit liabilities, asset reserves, leases, deferred revenue, state net operating loss carry-forwards and state general business tax credit carry-forwards.